Hey there reader 🙂 I’ve just submitted my first academic paper in a long time, on the world market for tuna and the law of one price. Here’s some of its content which didn’t all make the final paper, but also some of the literature review which was interesting but needed to be cut for the reasons of space

Introduction

Economic markets are magical things. The ability of competitive markets of willing buyers and sellers, transacting at arms-length from each other, to generate welfare-enhancing outcomes for both parties is unrivalled across different economic systems.

The Law of One Price (LOP), through market connectivity, is part of this economic magic. Prices in integrated markets will change together when supply and demand changes in either market, with sometimes surprisingly quick speed. How markets link depends on whether their products are complements or substitutes. The price change direction in both markets is unambiguously the same, which is why LOP is expressed with respect to price changes only, but the direction of the induced quantity change depends on the products.

Moving from the magical to the evidence-based, data-driven and concrete, this paper develops insights from the previous fishing LOP economic literature to test vertical LOP market integration between the raw and tinned tuna markets using UN Comtrade world import/export data across the period 2011-2024. The start of the paper goes through LOP with examples, and illustrations of its estimation for stationary and non-stationary data. Secondly, the existing fish-related literature is summarised, focusing on the motivations for the analysis, and the techniques used for LOP measure. Thirdly, the key insights from the UN Comtrade data are presented, together with the relative size of the two markets.

The relationship between raw tuna inputs and tinned tuna products is one of complements: increase supply of either should manifest increased supply in the other.

Theory of Law of One Price

Complements and substitutes

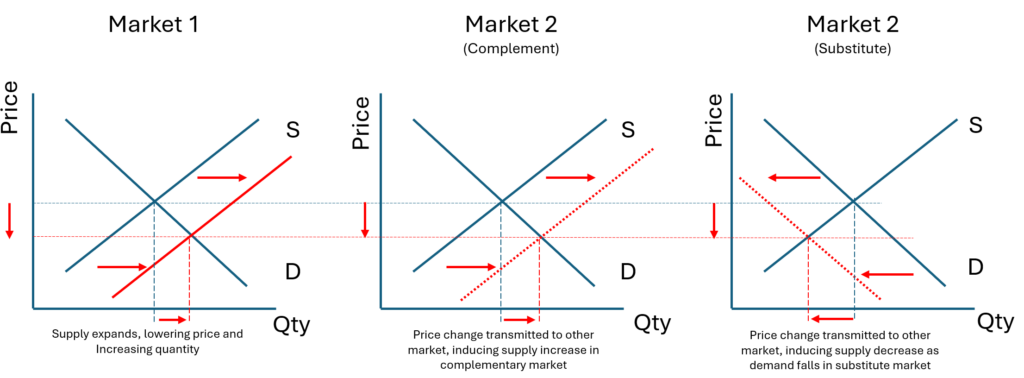

Figure 1 illustrates two interconnected market reactions, depending on whether the products are complements or substitutes to each other.

Figure 1: Initial and Induced Response

An expansion in supply in Market 1 decreases price in Market 1 which “transmits” into Market 2, inducing its downward price change. How supply in Market 2 responds depends on whether products in market 2 are complements or substitutes.

If Market 1 is the raw tuna market, and Market 2 is the complementary tinned tuna market, then a decrease in raw tuna prices together with an expansion in raw supply would induce a similar tinned tuna price decrease and an increase in the tinned tuna product quantities.

If, however, Market 1 was the raw market and Market 2 was the substitute chicken cutlets market, then an expansion of supply of raw tuna, with its price decrease would make tuna a more attractive protein source than chicken cutlets, leading to a fall in chicken cutlet demand, and a fall in both chicken prices and quantities sold.

The magnitude of the price change is itself a measure of the complementarity and substitutability of the products to each other. At most, the price in Market 2 can shift by the same percentage as the price in Market 1 (i.e., the LOP); however, smaller price shifts will reflect imperfect complementarity and substitutability.[1] The size of the quantity response induced in both the substitute and complement product markets depends on the supply and demand elasticities within those markets.

[1] (Asche, Gordon, and Hannesson, 2004) page 198-199.

Existing literature

There is a surprising wealth of fish-related Law of One Price economic research. Weirdly it mostly focuses on French white fish.

A Fish Is a Fish Is a Fish? Testing for Market Linkages on the Paris Fish Market (Gordon, Salvanes, and Atkins, 1993)

Gordon, Salvanes and Atkins’s research investigated a belief that high/low fish prices defined separate raw fish product markets.

The prevailing view at the time was high priced fish were sold in separate markets from low priced fish. Using data recorded at the Marche d’Interel National de Rungis in Paris, France – the largest wholesale fish market in Europe – they tested whether salmon and turbot – two high-priced raw fish species – were sold in separate product markets from cod, a cheaper fish.

Two real-world events motivated their work. Atlantic salmon production had been booming during the 1980’s, flooding the French markets with frozen salmon imports, and decreasing fresh and frozen salmon prices. Turbot and cod are wild-caught fish supplied primarily by the domestic French fleet and were considered a substitute for salmon. Cheap Norwegian salmon had secured a dominant market share of the France fresh and frozen salmon market.

Secondly, French retail channels were changing. Rather than selling fish predominately through restaurants, supermarkets were increasing their market share of fresh and frozen fish distribution. Both Norwegian salmon and French turbot were being sold through similar retail distribution channels.

If salmon and turbot shared a common market, then cheaper imported salmon was outselling French turbot in the more profitable premium market and undercutting the French domestic fishing industry. Also, the quantity of fish-farmed frozen Norwegian salmon released into the French market was controlled by overseas suppliers. Norwegian frozen salmon could flood the market when prices were high, and depart the market when prices were low. However, fresh caught French turbot would need to be sold at the prevailing market price, which was kept low by Norwegian supply change behaviour.

Results

All three fish prices were found to be I(1) and non-stationary. Using Johansen’s method, the authors found evidence of one cointegrating long-run equilibrium relationship between the prices of salmon, cod and turbot. However, the estimated Johansen cointegrating vector implied cod and turbot prices were related to each other, but salmon prices were both weak and strongly exogenous from turbot and cod prices.

Norwegian salmon did not share a common market with turbot and cod: cod and turbot shared one market; salmon had its own. At the wholesale level, cod and turbot could not be substitutes for salmon. Consequently, the Norwegian frozen salmon supply behaviour could not affect high-valued turbot, or low-priced cod.

High-priced turbot and low-price cod DID share a common market, but the authors did not test LOP’s validity in the turbot/cod market and estimate in Equation 1 to gauge the substitutability of premium turbot for cheaper cod.

On Prices of Fresh and Frozen Cod Fish in European and U.S. Markets (Gordon and Hannesson, 1996)

Gordon and Hannesson investigated both the long-run and short-run price relationships of whole fresh cod and frozen cod fillet imports across three European countries: France, Germany, and the United Kingdom (UK), as well as the geographically separate United States (USA). All four countries import substantial amounts of fresh and frozen cod product from Canada, Iceland, and Norway.

The USA had recently threatened trade action against Icelandic and Norwegian fish imports because of their whaling policies. The credibility of the threat depended on whether the USA sanctions could impose substantial economic costs on Iceland and Norway’s trade. If France, Germany, UK and USA shared a common cod market then cod fish prices would be integrated. Trade restrictions against Iceland and Norway would shock the price system, but the shocks would not be long lasting. Non-Iceland or Norway cod suppliers would respond to the price shocks and arbitrage across markets, diverting their trade into the USA. Correspondingly, Icelandic and Norwegian cod would sell into the other non-restricted France, Germany, and UK areas.

Short-run price shocks could not be avoided, but in a integrated market system, USA trade action would not have a significant impact on the price of fish, nor cause substantial damage to Icelandic or Norwegian trade.

Results

Gordon and Hannesson treated fresh whole cod and frozen cod as two products traded in separate markets which operated in different locations. For both fresh and frozen cod products, the price series were I(1) for all countries; however, later analysis using Johansen’s cointegration method suggested that USA fresh cod prices were I(0).

Fresh cod

For whole fresh cod, no evidence of cointegration of prices among the four countries was found. There was no support for long-run price linkages for fresh cod in the European and USA markets. There was also either no or weak evidence of market integration across the four countries. The authors were unsure, however, whether their results were true or from the statistical weakness of the more rudimentary Engle-Granger Two Step estimation procedure they used.

Dropping the USA fresh cod price, and re-testing for cointegration using Johansen’s method revealed one cointegrating vector for just the European countries. The USA and European markets for fresh cod were not integrated. Prices for fresh cod could deviate substantially from each other between the separate geographic markets.

Frozen cod

The authors were surprised to find only weak evidence for an integrated frozen cod market between the four areas. Despite the ease of transport for frozen cod, the evidence of market integration between Europe and the USA was not strong.

The short-run pricing dynamics were complicated, with French prices leading both UK and German prices. USA frozen cod prices had no short-run influence on European prices, and vice-versa. Only the ECT was significant in each country’s VAR.

USA trade action against Iceland or Norway – in the frozen cod market – was not a credible threat because of the long-run price linkages. USA action would have significant short-run impact on world frozen cod prices, but prices would eventually return to a common equilibrium between the countries. No measure of the “speed of adjustment” was reported.

Tests For Market Integration and the Law of One Price: The Market For Whitefish in France (Asche, Gordon, and Hannesson, 2004)

This paper contains the most complete outline of the theory of LOP and its applied estimation in the reported literature.

The authors chose to explore prices for whitefish products (cod, haddock, redfish, and saithe) in France. French fishermen derived a large portion of their income from these fish species and had organised into regional associations to represent their interests. The regional associations sort to stabilise, or increase, fish prices and fisher incomes.

If the whitefish market was integrated, then regional associations would find it difficult to permanently lift prices in their areas. If frozen cod fillets were also integrated with fresh whitefish prices then an integrated international whitefish market would undermine the regional association’s price control efforts.

Modelling multiple integrated product markets

Referencing Equation (1) in this paper, that equation could be extended to any number of goods in different geographical markets. However, adding more products in markets does not add additional information to the analysis. If the different prices are cointegrated, then they will all be driven by a common stochastic trend. When estimated as a system of prices, the system should have n-1 cointegration vectors. Therefore, no structural information would be lost through reducing the modelling to only bivariate relationships between the prices.

Multivariate price models are, however, of interest for at two reasons.

- With n data series, there can at most be (n-1) cointegration vectors. However, there are ( n^2 – (n/2)) possible pairs of prices. All but (n-1) pairs will be redundant.

- Different conclusions might be obtained depending on which pairs are chosen for applied work. This problem is avoided in a multivariate specification, as only (n-1) cointegration vectors could be derived

2. Unfortunately, multivariate systems are sensitive to the dimensionality of the estimated system.

- The reliability of the results decreases with the number of parameters estimated from a fixed set of data observations. This is “the curse of dimensionality”.

There is no clear answer as to what the correct strategy is. The authors suggests bivariate models should be initially estimated since they contain all the relevant structural information. Multivariate models could then be estimated to refine the results.

Results

All prices were tested and treated as I(1) and modelled as different combination of price pairs which were all cointegrated. The results suggested the different whitefish species, except redfish, could all be treated as one single “whitefish” product type.[1] A long-run stable equilibrium relationship operated between cod, haddock, redfish, and saithe prices with cod as the price-leader.

There was one frozen fillet whitefish market in France that includes cod, haddock, saithe, and redfish. The relative prices of frozen fillets of cod, haddock, and saithe satisfied the LOP. The species so integrated, they could be treated as a single species with a single price. Redfish was the exception, and its prices did not satisfy LOP.

The author believed that, together with market integration results reported elsewhere, there existed a world market for frozen cod fillets; therefore, one global market for frozen whitefish fillets. The French regional fishing associations efforts would ultimately be in vain.

[1] These results also provide evidence that the market segments for cod, haddock, and saithe are so highly related that the three species can be aggregated into a single good due to the generalized composite commodity theorem. If cod, haddock, saithe can be aggregated into a single good, then each species supply curves must respond in the same manner and same direction as described for complement products in Figure 1. If all were not compliments, and some were in fact substitutes, then despite their prices moving strictly together their catch quantities would show divergent quantity changes. With prices moving consistently in a common direction, but quantities potentially not moving in common directions, then the species catch proportions – the implicit “whitefish” composite commodity baseweights – must also be changing over time, affecting the aggregated commodity’s composite quantity measure.