I’ve previously written about how the US Dollar is the ultimate IOU: the USA seems impervious to monetary crisis. The US Government seems to be able to continuously borrow from the world running some weird sort of international ponzi scheme where it keeps issuing more debt, and international creditors keep being willing buyers for increasing amounts of US Government debt.

The effect is that the US has never had to reduce its government expenditure or increase taxes to pay for previous US government spending. It has always been able to roll over its repayment obligations issuing increasingly more debt, which is why I’m calling it a ponzi scheme. Every other country’s government, when it continually spends more than it earns (not just every now and then in a bad year) they ultimately get itself into a monetary crisis: a point where no lender want’s to roll over their debt, and the government defaults on its financial repayment obligations. Wikipedia has a list of them. Mexico and Argentina are the main culprits who spring to my mind, but as Wikipedia shows, you don’t need to be a Latino government to handle your government finances badly.

A bit more about Money…

Unlike you and I, when governments get sloppy with their finances, they have four additional options you and I don’t have.

They can:

- “Spark up the printing presses” (which literately happened in Zimbabwe between 2007 – 2009) print money, and pay their bills with wheelbarrows of cash,

- Do some “Quantitative Easing”, which is the electronic equivalence of sparking up the print presses through adjust the balances in settlement cash at the Reserve Bank and paying their bills with newly made balances in their RBNZ account,

- Lean on their sovereign rights to tax their subjects, and borrow against that future right from private and international institutions. Spending now implies increased taxes (or decreased government services) in the future. Sovereign countries can borrow against this power, and issue bonds now against the power to tax in the future.For example, in New Zealand’s case between May 2023 and May 2024, the New Zealand government issued a net (issues – redemption) $NZ 21 billion of debt. Between May 2024 and May 2025, it issued a further net $NZ 25 billion of debt. In total, the New Zealand Government has $211,658 million worth of debt mostly held by the Banks and Non-Residents. With New Zealand’s Gross Domestic Product (GDP) sitting at $430,000 million as at March 2025, New Zealand’s Government Debt is 49% of the country’s GDP.

However, “we” (the taxpayer) know that in order to pay back $25billion worth of services we are receiving now but not completely paying for now in taxes, we’ve got to pay additional taxes in the future, or decrease the future volume of government services we would have received to pay for todays spending.

There’s no free lunch, you either pay for it now, or you pay for it later. The “trick” the politicians play is the make the length of the debt so long that one generation (who vote for the current government) receives the higher services now, and future generations (who currently do not vote for the current government) pay the cost through receiving less services in the future. In New Zealand, this is exactly what’s happened with education and housing. Prior to 1990, tertiary education was free, now its very much not free, and students incur sizable debt. The Boomer Generation have benefited from their higher educations without paying a cost.

During the 1960’s, the Government subsidised housing loans through below market cheap interest rates. Now, there’s no such thing. But the Government will “graciously” allow first-home owners to draw on their own savings which has gone into a Kiwisaver scheme. But Kiwisaver is still only the first-home owner being “allowed” to use what is still their own money.

Its not always about the Boomers screwing over Millennials and Generation Z. If government borrowing is used to create infrastructural assets that span generations, then its fair that the cost is spread over generations. Things like roads, airports, hospitals, electricity grids.. blah blah blah. Its when government borrowing funds current spending, like health care expenditure, superannuation, or current services that do not generate assets that intergeneration equity becomes an issue around the quality of how the borrowed funds have been used.

… yes New Zealand Politicians, that is a very pointy stare I’m giving you, looking at the poor quality of how you’ve spent $25 billion of debt on current services this year…

- Use their sovereign powers to tax, and increase taxes on the economy, right here, right now and not through future lending. This is actually taxing the citizens now, or actually decreasing services now. However, this is normally very unpopular with the people, and a fast way to becoming thrown out of Government via the next election or, in some cases, revolution.

When governments take the third option the issued debt turns up as new balances in their Reserve Bank bank accounts ready for them to spend. Bonds sold to the Rest of the World, its “sorta” like printing money because it represents new liquidity entering New Zealand. When bonds are purchased from the Banks (as $NZ65,095 million is in New Zealand’s case), it’s not like “new money”, because that was money was already slushing around New Zealand before making its way to the government. That money has just been diverted by the banks from being lent to the household sector predominately through mortgages (where most of New Zealand’s private sector debt normally goes) to the government. When domestic agents purchase the debt it isn’t new money – its cash that was already slushing around in New Zealand,

The important thing though is that lending from the Rest of the World is new money to New Zealand, because its origin came from somewhere else. Yes, the government has taken on an obligation to repay that money in the future (plus interest), but in return for writing an IOU, it gets money it can spend, spend, spend, with right now. And that’s what makes government debt, when financed externally, all inflationary like turning on the printing presses, or quantitative easing.

What’s up with America?

Trump’s continued a modern(ish) legacy of spending lots more than the US government receives in taxes and other revenue with his Big Beautiful Bill Act. I’ve got to admit – I quite like the Act’s name 🙂

But here’s a little official US Government website which puts it into context: https://fiscaldata.treasury.gov/americas-finance-guide/national-debt/ together with some interesting eye-candy:

Here’s another Treasury.gov website that gives the Debt to the Penny: exactly $36,213,797,741,182.40 as of 2 July 2025.

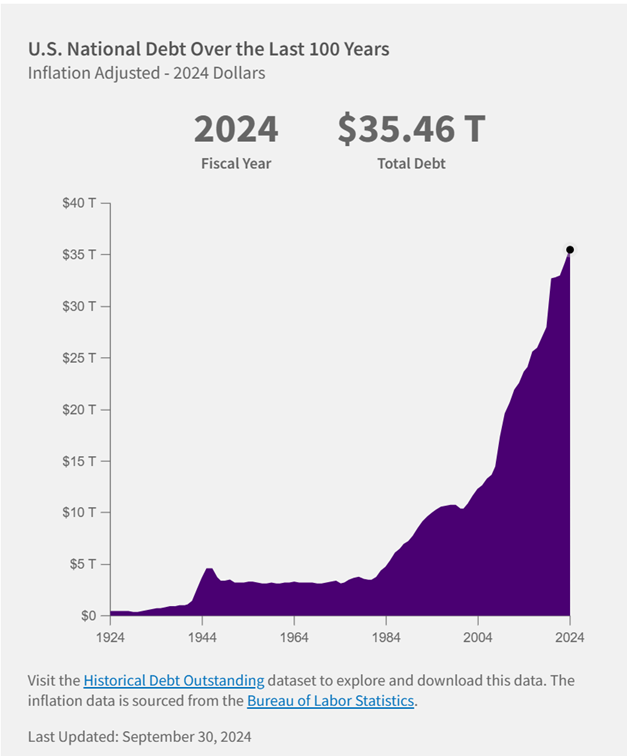

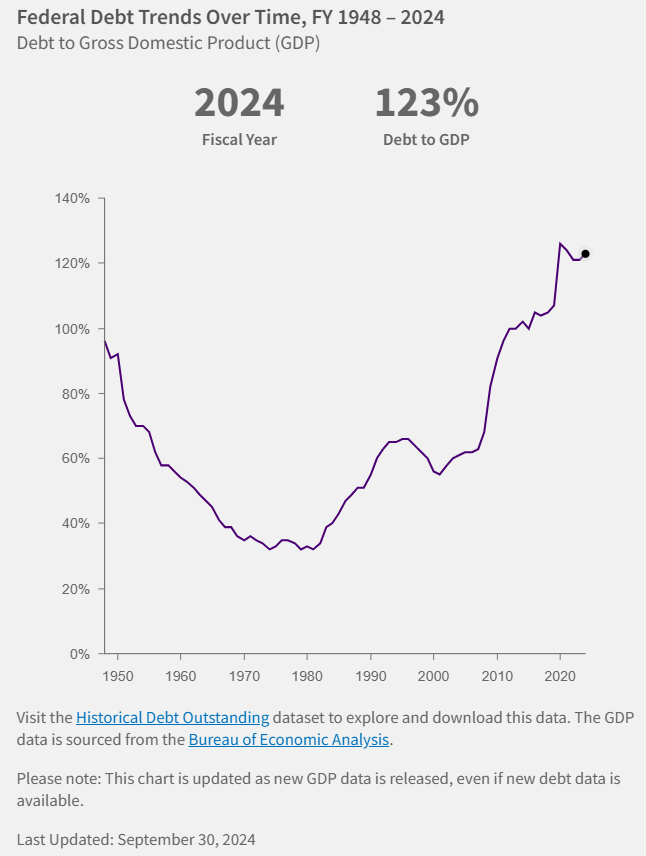

While a stunning graph, if the US economy is growing, then taking on debt is “ok” – the government has an increasing ability to pay the debt, because it can tax economic sectors whose incomes are also increasing in a growing economy. It’s this one – where growth in debt is compared against the growth in the economy generally – that’s really bad:

As of 30 September 2024, if the US government tried to pay back the debt through increased taxes, the amount of the US Government debt exceeds the amount the strongest world economy can generate in a single year.

Of course, you could say that of course the debt wouldn’t be expected to be paid back in a single year, and that’s true. But it also depends on the maturity of the debt – is it short term, or long term debt? Unwind that debt mountain, and repaying it over time depends on how much time lenders will accept.

International Debt Market Impacts

It wasn’t easy to find ready stats, but I found this comment from a Canadian Bank noting that the effect of having to pay higher interest to persuade buyers to purchase more US debt would lead to increased interest costs for Canadian debt as well. While the US Treasury has taken steps to not dump the US debt on the market all at once, the effect of more US debt means a permanent upward pressure on Canadian government interest rates:

The bond market is bracing for an extraordinary supply challenge. Roughly $9.2 trillion in U.S. Treasuries—about one-third of all outstanding marketable debt and nearly 30% of U.S. GDP—will mature in 2025, and an estimated 55–60% of it falls due before July. When the Congressional Budget Office adds a $1.9 trillion federal deficit to that stack, gross issuance climbs above $10 trillion—an amount no modern market has absorbed before.

…

Put simply, if Washington pays more to roll its debt, Ottawa and Canadian households usually end up paying more, too.

…So, will the $9 trillion wall force rates sharply higher? Probably not in a disorderly fashion, but it almost certainly anchors yields in a higher range.

May 8, 2025